Case Study: Optimising ALAMI Funder Registration with OCR Technology

- Pratiwi Nur Amini

- May 4, 2025

- 7 min read

Updated: Jun 4, 2025

🤔 a little back story and the problem:

In late 2019, ALAMI introduced its peer-to-peer lending app, aiming to facilitate connections between lenders and borrowers for SME financing in Indonesia. During that period, the registration funnel and KYC process were impractical, being handled and reviewed manually by frontline operational staff. Consequently, ALAMI achieved only a 4.5% success rate in their registrations, with a service level agreement (SLA) extending up to 3.5 hours. Additionally, users complained about a lengthy onboarding process, reporting it took around 3 working days from registration to becoming verified funders.

My Role | Product designer (conception, visualization, interaction, UX and UI Design, Testing, Prototyping, coordinating with developers and PMs, pitching to stakeholder) |

Team mates | Mahardhika Sulistyo (Direct Lead), Sukmayanti (PM), Sefrina Zafira R. (Product Researcher), Diosi J (Illustration Designer), Safira Ardya P. (UX Writer), Nurhadi Wibowo (Mobile Engineer), Hadyan P. Y (Backend Engineer) and other engineers |

Key Expert/Stakeholder | KYC, Ops, Customer Service Team and ALAMI P2P apps users |

Dates | January - April 2022 |

Sector | Financial Technology |

🎯 Goals:

Optimized the onboarding flow for the ALAMI Mobile App 2.0’s Peer-to-Peer experience, aiming to create a more seamless journey and significantly improve user conversion.

Implemented automated document verification using OCR (Optical Character Recognition) for ID cards, identity validation, and biometric authentication, successfully streamlining the verification process and reducing overall waiting time for retail funders.

🎨 Design Process:

We followed the User-Centered Design process to investigate how our users behave during registration and how they complete it. We also dove into our customer service and KYC teams’ struggles in guiding users through the registration process. Letting users, the CS team, and the KYC team guide us, we brainstormed and designed multiple solutions. We then tested our ideas through usability testing and developed a high-fidelity interactive prototype based on our findings.

👀 Research:

😎 Competitive Analysis

To begin our research, we analyzed four direct competitors in the P2P lending and financial startup space that have implemented OCR technology in their registration process: Investree, Modal Rakyat, Akseleran, and KoinWorks.

We found that all four platforms have already adopted OCR to streamline their user onboarding. The required documents typically include a KTP, passport, or driver’s license, as well as a Tax Identification Number (NPWP) and a selfie for facial verification.

The standard SLA (Service Level Agreement) from registration to becoming a verified funder is typically instant or completed within the same day (60 minutes), with no working days required. However, in cases where the user is flagged as a high-risk individual, the process may involve an additional manual verification phase conducted by the operations team.

We also conducted interviews with our subject matter experts from the KYC, Customer Service (CS), and Operations (Ops) teams to understand the challenges they face in guiding users through the onboarding process. Several key issues emerged when OCR technology is not implemented:

Longer Registration Time and Higher Drop-off Rates: Without OCR, users must manually input their personal information such as name, ID number, and tax identification number. This process is time-consuming and prone to user frustration, which often leads to incomplete registrations or form abandonment. As a result, the overall conversion rate from new sign-ups to verified funders significantly decreases.

Higher Risk of Human Error : Manual data entry increases the likelihood of mistakes, such as typos in ID numbers, mismatched data between forms and uploaded documents, or missing fields. These errors can cause the verification process to fail and require manual intervention from the KYC team, which slows down the onboarding flow and increases operational workload.

Increased Burden on Ops and CS Teams: In the absence of OCR, the Operations team must manually verify every submitted document, compare it with user input, and ensure accuracy. This slows down the approval process and makes it harder to scale the team efficiently. On the other hand, the CS team experiences a higher volume of support inquiries due to user confusion, delayed verification, or unclear rejection messages, resulting in longer response times and a less satisfying user experience.

Compliance and Fraud Risks: Manual onboarding processes are more vulnerable to oversight. Important risk indicators may be missed, KYC procedures may become inconsistent, and the ability to respond quickly to fraud is reduced. These gaps can lead to non-compliance with regulatory requirements (such as those mandated by OJK in Indonesia), potential financial penalties, and long-term reputational harm.

🚧 Research Synthesis:

Based on user and internal team insights, ALAMI needs to focus on the following:

Implement OCR to Automate Data Extraction: Integrating OCR will significantly reduce the need for users to manually type their personal information, lowering error rates and improving user satisfaction.

Simplify and Clarify Document Submission: Provide clear guidance on what documents are required, how to upload them correctly, and acceptable formats. A progress bar or checklist could help manage expectations.

Provide Real-Time Feedback and Status Updates: Introduce a system that gives users real-time updates during each step of the verification process, e.g., “KTP received,” “NPWP verified,” “Awaiting selfie match,” etc.

Reduce Manual Bottlenecks: By automating the verification process with OCR and facial recognition, the Ops and KYC teams can focus on edge cases or high-risk users, allowing most users to onboard quickly without delay.

🧑🎨 Ideate and Design:

Before jumping into sketching, we first needed to map out the user flow, detailing each step users take to register and complete the onboarding process in the ALAMI app. This flow served as the foundation for identifying pain points and designing a smoother, more intuitive experience.

This includes the splash screen, four USP screens (to clarify that ALAMI is not a personal loan app), an optional funding simulation, and a registration form (email, password, and name).

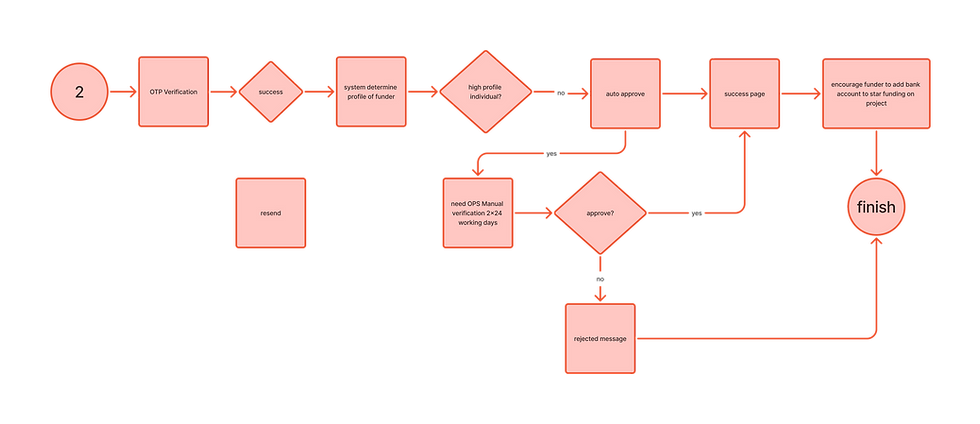

Step 1 Continue to complete additional data. This is where OCR will take part

Step 2 At this stage, the funder is assessed based on their profile. If they are classified as a high-risk individual, additional manual verification by the Ops team is required. Otherwise, the funder is successfully registered.

step 3

Sketching:

🧡 Designing Process

I translated my sketches into high-fidelity mockups using Figma, ensuring that each entry point was thoughtfully crafted to avoid causing user confusion. During this stage, I collaborated closely with the UX writer, as P2P lending platforms like ALAMI are often misunderstood as individual loan apps. It was essential to ensure that every piece of information clearly and firmly communicated that ALAMI is a funding platform.

Since there are many pages involved, I would like to emphasize that the design showcased here focuses solely on the OCR flow.

🧪 Usability Testing

I narrowed down potential ideas and began prototyping based on the flow outlined in the service design blueprint. Our product researcher recruited four participants, three under the age of 35 and one over 35, to test the prototypes. (Participant names have been fully blurred to protect their privacy.)

For usability testing, our product researcher applied two key evaluation methods: Heuristic Evaluation (HE) and the Customer Effort Score (CES).

Heuristic Evaluation is a usability inspection method used to identify design issues related to the user interface. It is an effective approach for diagnosing problems early in the design process and ensuring the product stays aligned with usability best practices.

Meanwhile, the Customer Effort Score is a customer feedback metric that measures how easy it is for users to interact with a product or service, rather than overall satisfaction. Participants were asked to rate the ease of use on a scale from 1 (very easy) to 6 (very difficult), providing insights into how intuitive and seamless the onboarding experience felt from the user's perspective.

summary Customer Effort Score (CES) :

Registration Process: 2 Easy

Completing the Document (OCR) : 2 Easy

Completing Bank Account : 1 Very Easy

as for HE Metric, our product researcher carefully laid down the recommendation and area we should improve:

✨ Final Design:

Our final design is structured into four key phases that users must complete:

App Reassessment: Users are first asked to reassess and determine whether ALAMI is the right app for them. This step helps prevent misconceptions—particularly from users who might mistake ALAMI for a consumptive loan application.

Initial Data Submission: Next, users are required to submit their basic information—email and phone number. This step helps us filter out unqualified or incomplete submissions early in the process.

Document Verification (OCR): Once the email and phone number are validated, the OCR (Optical Character Recognition) process begins. In a single, real-time session, users must upload a photo of their KTP, NPWP, and a selfie to ensure identity verification.

Final Data Entry and OTP: In the final phase, users must complete additional data fields and input an OTP (One-Time Password) to officially submit their application.

There are numerous screens involved in this flow, but for now, I’m sharing just a sneak peek of the overall user journey. Take a look:

🚀 Results and takeaways:

Since the feature was fully rolled out on December 20th, 2022, only 29 out of 182 user submissions required manual verification, meaning approximately 84% of the data successfully passed through OCR, significantly reducing the backlog for the KYC and other team involved. Horrayy 🎊🙌

💬 Reflections:

This project was a significant learning experience for me, both professionally and personally. As one of the main designer on the OCR onboarding initiative, I had the opportunity to lead the end-to-end design process, from research and ideation to prototyping and testing. It taught me how to manage cross-functional collaboration effectively, communicate design decisions clearly, and present ideas confidently to stakeholders, engineers, and other teams involved.

I also gained a deeper appreciation for the critical role of UX in financial products, especially those operating within strict regulatory environments. A reliable, well-crafted user experience isn’t just about usability, it’s essential for maintaining trust, ensuring compliance, and supporting operational efficiency. This project reinforced how thoughtful design can bridge the gap between user needs and business goals.

Comments